Jeffco Schools’ Out of Control $705 Million Capital Program, Chapter Two: The Scandal Has Widened and Worsened

The Jefferson County school district is located in the western suburbs of Denver. It is the nation’s 37th largest district, serving about 84,000 students with annual revenues of over a billion dollars a year.

Jeffco has a population of almost 600,000. Many of its citizens are educated and affluent — 42% of adult residents are college graduates, and median household income was $85,890 in 2018.

On 7 October 2020, I published a detailed, evidence-based analysis of Jeffco’s $705 million six-year capital improvement program that was approved by a razor thin 0.24% margin in November 2018: “Jeffco Schools’ Out of Control $705 Million Capital Program: A Case Study in Poor Management, Weak Governance, and Dysfunctional Culture.”

This report updates that analysis through early February 2021. It covers the following topics:

1. New Developments in Chronological Order

2. The Kathleen Askelson Report: Spin City with Evidence of Election Fraud?

3. Did the Rating Agencies Really Say What Steve Bell Claims They Did?

4. Conclusion

New Developments in Chronological Order

7 October 2020: At the scheduled Jeffco Board of Education quarterly meeting with the Citizens’ Capital Asset Advisory Committee (none of whose members showed up!), Board Director Miller read a statement expressing her deep concerns about the Capital Improvement Program, and called for the appointment of an independent outside firm to conduct a performance audit of it.

Miller began her career as a municipal Ratings Officer at Standard and Poor’s. She was later a public finance investment banker at Kidder, Peabody, and then a management consultant specializing in large project development. Currently, Miller’s firm advises school districts around the country on enrollment, strategy, facilities planning, financing, and project management. She also holds a SEC/Municipal Securities Rulemaking Board Series 50 Municipal Financial Advisor License.

Here is her statement in full:

“Back in November 2018, we asked the community to support a $567 million dollar bond ~ 5B, to upgrade aging buildings, provide new furniture, new labs, and new schools throughout the district. We promised our community and our bond investors that the Citizens Capital Asset Advisory Committee [CAAC] would faithfully oversee the capital program, including financial oversight as well as the on-budget delivery of all the projects that were promised to our voters.

Last January, you and the other members of the Capital Asset Advisory Committee joined us and you said, “it is very important for us to make sure that each facility gets what it is promised. We cannot make changes to what was promised. Those items that are on the bond have to be followed exactly the way they are, and come in under budget.”” Speaking for many Jeffco voters, I could not agree more.

When we sold the bonds in December of 2018, we benefited from a very strong market and secured an additional $50 million in bond premium, which is basically an unexpected windfall, a bonus so to speak, that could be spent on additional projects. In Denver, Poudre and Thornton, which also benefited from a strong market, those districts had their bond oversight committees make recommendations to their school boards about how best to use the extra money they received from the sale of their bonds. And those boards voted to allocate the extra money to additional projects that were high priorities for their communities.

The Jeffco community has been denied the chance to have that discussion. We didn’t have the chance to ask the community where it wanted to address equity challenges. We never had the opportunity to fund new labs for Jefferson High School, nor new schools to replace the old ones in the areas of Jeffco facing the greatest challenges, nor address overcrowding issues at Ralston Valley, nor consider upgrades for Outdoor Lab. Those discussions never happened. I asked for them, and I was dismissed.

But the committee [CAAC] did raise the issue of the extra $50 million dollars realized in the sale of the first round of bonds. On May 7th 2020, the committee asked Tim Reed, in front of our CFO, Kathy Askelson, our COO, Steve Bell, and other members of our Finance Team (Stephanie Corbo and Nicole Stewart) who was responsible for allocation of the bond premium? According to the meeting notes, Mr. Reed stated, and I quote, “THE USE OF PREMIUM AND ANY DISTRIBUTION IS A BOE DECISION NOT THIS DEPARTMENT.” Mr. Reed also promised to raise this issue with this Board.

Twelve hours later, that SAME day, as we discussed the 77% cost overrun at Alameda High School, I asked Mr. Reed if any of the $50 million bond premium had been spent. Initially Mr. Reed denied the unauthorized use of the bond premium, but then admitted that it “had not been spent in its entirety.” At no time did he bring forward what he told the committee [CAAC] just twelve hours earlier, that how to spend that extra $50 million, that bonus money, was a board of education decision. But then Kathy Askelson, Stephanie Corbo, and Nicole Stewart, nor Steve Bell didn’t say anything to the board either.

That’s a very big problem for me and for this district. As board members we have a fiduciary duty of care. We promised our taxpayers and bond investors the greatest level of transparency and oversight of the $705 million dollar capital plan, that included 5b approved by the voters. It is painfully clear we have not kept that promise.

Therefore I ask that we abide by the resolution language the previous board approved on September 6, 2018. The resolution stated “…the spending of the proceeds of such debt to be monitored by the Citizen’s Capital Asset Committee and subject to an independent annual audit.”

I ask this board to call on the audit committee to secure an independent performance audit, as other large schools districts have done across the country for their capital programs. We must be completely transparent with the citizens of Jefferson County and with our bond investors about the implementation of this capital program. To do any less would be a betrayal of their trust.”

Directors Susan Harmon, Ron Mitchell, Brad Rupert, and Stephanie Schooley refused to support Miller’s motion.

9 October 2020. After she resigned as Jeffco’s CFO at the end of August 2020, Kathleen Askelson was hired as a consultant to the district. A report she submitted to the district on 21 January 2021 states that, “An interim report on the bond program was requested on October 9, 2020.” That’s just two days after Harmon, Mitchell, Rupert, and Schooley failed to support Miller’s motion for an Independent Performance Audit (a specified term under Government Auditing Standards — see Chapters 8 and 9 of the “Yellow Book” published by the Government Accountability Office (GAO).

Strangely, Askelson did not say who requested her report.

This report was sent to members of the CAAC on 21Jan21. The notes to the CAAC meeting on that date say that the report was requested by the Board of Education. However that is not true; there is no record, in writing or in the meeting videos, of the Board ever having made such a request, particularly after having just rejected Miller’s motion for an Independent Performance Audit.

I submitted multiple Colorado Open Records Act (CORA) requests in an attempt to determine who requested Askelson’s report. Almost all of them were either rejected or came back with a demand for ridiculous fees before the district would even search for the information I requested (and those fees were non-refundable if no information was found).

However, I did receive an answer to my CORA requesting the consulting invoices Askelson has submitted to Jeffco. These billing records are in the Evidence Appendix, which can be downloaded using the link at the end of this report.

As you can see, there is no mention of the “Bond Report” in the October Statement of [Consulting] Work Askelson and Jeffco’s Chief Human Resources Officer agreed she would perform in October 2020. The “Bond Report” was added later.

On 9 October (the date Askelson says the Bond Report was requested) only one meeting is listed in her invoices: A “planning meeting” with Acting Superintendent Kristopher Schuh, District Chief of Staff Helen Neal, and Acting CFO Nicole Stewart.

14 October 2020. Askelson’s billing records also note another meeting five days later with Schuh, Neal, and Stewart. However, this time they were joined by Jeffco’s Chief Operating Officer Steve Bell (who is in charge of the Capital Improvement Program) and Board Chair Susan Harmon. The purpose of the meeting is described as “project work and outcomes.”

In her report, Askelson notes that the following objectives “were defined” for her work (but again does not say who defined them, or when they were defined):

· “Review the original bond plan by project as communicated to the community and validate the projects developed in the PeopleSoft system (district financial system) and construction reports reflect the same budgets.

· Review of the current revised budget identifying the changes from the original budget and subsequent use of contingency.

· Review of current contingency balances.

· Review overages from current budget to actual costs.

· Make recommendations for changes in processes or communication to the Capital Asset Advisory Committee (CAAC) and/or Board to be included.”

Note that there was no instruction to Askelson for her to follow Government Auditing Standards for Independent Performance Audits when preparing her report. That is not surprising. Having been so deeply involved with the Capital Improvement Program, it would have been impossible for Askelson to meet them.

5 November 2020. Just when you think this story can’t get any worse, it does. The Consent Agenda for the 5 November meeting of the Jeffco Board of Education included a contract for more than $500,000 for Calahan Construction, with which Gordon Calahan is affiliated. He is the only citizen who is a member of both the district Financial Oversight Committee (FOC) and the Capital Asset Advisory Committee (CAAC). Both these are advisory committees to the Board of Education, and play a critical role in the district’s governance process.

Per both the Proposition 5B language approved the Jeffco voters in the November 2018 election, and the Official Statement provided to investors in the district’s bonds (which incorporates the 5B language by reference), the CAAC is supposed to provide voters and bondholders with independent oversight of Capital Improvement Program spending.

Subsequent investigations (using Jeffco’s financial transparency database) revealed that Calahan’s company has received more than one million dollars in contracts from Jeffco’s Capital Improvement Program.

It is hard to understand how the CAAC can provide “independent” oversight over a $705 million dollar Capital Improvement Program when at least one of its members is receiving Capital Improvement Program contracts awarded by the very district staff they are supposed to be overseeing. This is a blatant conflict of interest and, many would argue, a clear violation of the fiduciary duty of loyalty.

Calahan’s presence on the CAAC also makes a mockery of this district requirement for the Citizens Capital Advisory Committee: “Members must be free from any relationship that would interfere with independent judgment.”

In advance of the 5 November meeting of the CAAC, I sent an email to Acting Jeffco Superintendent Kristopher Schuh, Board Chair Susan Harmon, and members of the media describing my concerns with respect to the Calahan contracts. I also noted that since questions had been raised about the management and oversight of the Capital Improvement Program, both the FOC and CAAC had begun to violate the Colorado Open Meeting Act, by not making it clear at least 24 hours in advance how members of the public could attend their meetings.

The notes from the 5 November CAAC meeting show that the email was discussed. The result was depressingly telling with respect to the extent of the rot in Jeffco’s culture.

First, Chief Operating Officer Steve Bell misrepresented my complaint, describing it as related to Calahan having inappropriately obtained contracts, rather than the fact that he had obtained them at all while still a member of the CAAC.

It was also telling (but not surprising) that members of the CAAC voted against asking for an Independent Performance Audit, as such an audit would almost certainly be highly critical of their own performance in providing independent oversight over the spending of bond funds that the CAAC is mandated to provide by the language of Prop 5B (on behalf of taxpayers and bond investors).

There were also other odd but interesting items in the notes from this CAAC meeting (notes are in the Evidence Appendix):

“Tim Reed sent an email 10/16, to CAAC members that noted that certain individuals are questioning the Capital Improvement Program progress, financial status and by implication CAAC is not providing adequate oversight of the Capital Improvement Program. In the email there were suggestions for consideration and discussion at today’s meeting.”

In light of this, it is particularly strange that the members of the CAAC were not informed by any member of management (nor by Kathleen Askelson, who also attended) that Askelson had already been commissioned, apparently by Schuh, Stewart, Bell, and Harmon, to write a report about the Capital Improvement Program. That is a strange omission, to say the least.

These other exchanges were also interesting:

“Megan Castle asked if the Board of Education was looking at the bond language itself and what the citizen advisory committee’s responsibilities are. She would like clarification on what oversight means? With the 10/16 email the responsibilities and requirements of members was included. Is the committee doing what they are supposed to do? Performance audit, what does that mean for CAAC?”

Two years after Prop 5B promised voters and bondholders that the CAAC would provide independent oversight over the spending of bond proceeds, “M.L. Richardson stated that she would like the following information provided to CAAC along with definitions:

· Scope of work

· Cost

· Variation to the scope of work

· Cost of variation, increase or decrease

· Final cost

· Source of funding

· Bond premium breakout

· Definitions: bond funding, program and bond contingency, capital transfer

· Explain exactly what the source is”

In response to Richardson’s request, “Tim [Reed] stated that all the CAAC reports, presentations and meeting notes are on the Jeffco public website.” Could he have been more arrogant and dismissive of Richardson’s wholly reasonable, if far too long delayed, request? Reed told members of the CAAC that if they wanted to obtain the information they needed to exercise independent oversight over the Capital Improvement Program, they would have to root around on the Jeffco website to find it!

Finally, the contemptuous treatment of the CAAC by Bell and Reed was painfully summed up in this passage from the meeting notes:

“Jeff Wilhite proposed that a review of the bond contingency be performed to focus on preparing information to be presented to the BOE on how the contingency has been used to this point in the bond program. Jeff proposed that he, Megan Castle, George Latuda could make up this team. There was no discussion from the remaining members of the CAAC on moving forward with this proposal. The suggestion has been taken under advisement [by Bell, apparently].”

This is exactly the activity that Proposition 5B requires the CAAC to perform. And Bell prevented them from doing so, making it painfully clear that the committee charged with providing independent oversight is actually run by Steve Bell (the CAAC doesn’t even have a citizen chairperson). Think about that.

Note too that all these statements were made in the presence of Board Member Brad Rupert, who attended the CAAC meeting, and who, according to the notes, did not object to anything Bell or Reed said. What does this tell you about Rupert’s view of how a billion dollar school district should be governed? Or about the language in Prop 5B?

11 November 2020. One item on the agenda for the 11 November board meeting was a regular quarterly review with the members of the Financial Oversight Committee (FOC) to discuss whether Prop 5A funds had been used as specified in the resolution voters approved in November 2018.

Recall that in my previous report, I noted serious issues related to the use of operating funds raised in accordance with 2018’s Prop 5A that were dedicated to expanding STEM and CTE programs being used for capital expenditures. Specifically, their use to pay for capital costs related to the construction of the new Warren Tech South School.

Only one member (who was just appointed) of the FOC showed up to this board meeting, either in person or via videoconference.

As was the case at the CAAC’s last meeting with the board, the FOC’s presentation was given by the person over whose work the FOC is supposed to provide oversight — in this case, Nicole Stewart, the district’s CFO.

Board director Susan Miller noted that, based on the FOC’s meeting notes, it did not appear to have discussed the use of 5A operating revenues intended to support STEM and CTE programming to build a building at Warren Tech South. Moreover, this use of funds was strangely omitted from the spreadsheet of 5A fund uses that the FOC supposedly reviewed before giving it to the Board.

As has frequently been the case since Director Miller began to publicly ask questions about the management and governance of the Capital Improvement Program, Board chair Susan Harmon cut off the discussion. Board director Mitchell then admonished Miller for “not trusting management.” So much for board directors of a billion dollar organization exercising (or perhaps even aware of) their fiduciary duty of care…

Later in the meeting, Miller made two motions.

First, that the board retain an outside firm to conduct an independent performance audit of the Capital Improvement Program. Board members Harmon, Rupert, Mitchell and Schooley again refused to support it.

Once again, Harmon said nothing about the report that Askelson had been working on since 9Oct20, which was allegedly requested by the Board. Rather strange, don’t you think? Especially since Harmon appears to have been present at the meeting when the design of the report was agreed?

Miller’s second resolution noted the board and district’s frequently mentioned concerns with equity, and how district schools with high percentages of at-risk students were mostly in worse condition than those with lower percentages.

With that in mind, and given the previous uses of Bond Premium funds that were not authorized by the Board, Miller proposed that the use of any Bond Premium received after the district’s upcoming second issue of Prop 5B bonds must be expressly approved by a public vote of the Board of Education (as is the practice in other districts, such as Denver and Poudre). Again, Board members Harmon, Rupert, Mitchell and Schooley refused to support Miller’s motion. Why? Who benefited from their refusal to back this motion?

1 December 2020. Meeting of the Financial Oversight Committee. Per the notes from this meeting (see the Evidence Appendix), Paul Niedermuller, from Jeffco’s independent auditor, Clifton Larson Allen, LLP, “advised [the FOC] that a correspondence was received from a citizen regarding auditing of the bond program.

“He noted CLA has a firm policy to not engage with citizens, thus the communication was referred to the Financial Oversight Committee Chair. He noted that the capital program is audited as part of their engagement to audit the financial statements of the district; anything beyond that [such as an Independent Performance Audit conducted in accordance with Chapters 8 and 9 of the GAO’s Government Auditing Standards] would require a separate engagement.”

“Stewart noted that the Capital Asset Advisory Committee (CAAC) had received the same letter and that the district is working internally to provide more clarity to the CAAC to assist them with their reporting to the Board.” Note that this is only happening TWO YEARS after bond proceeds were received by Jeffco, spending on the Capital Improvement Program began, and after Jeffco had received multiple whistleblower communications.

The meeting notes continue, “In response to a question regarding if the audit by CLA complies with the required language of the bond, Niedermuller clarified that they look at financial costs for compliance as part of the annual audit of district financials. He confirmed that CLA did not have specific direction to do a performance audit which is different than the financial audit.”

Note that, despite their awareness of the issues being raised with respect to the management of the Capital Improvement Program, as well as district compliance with the Prop 5B language that promised Jeffco voters and bondholders that an annual “independent audit” would be conducted covering the use of bond funds, per the meeting notes NOT ONE MEMBER OF THE FOC QUESTIONED WHETHER AN INDEPENDENT PERFORMANCE AUDIT WAS NEEDED.

This continued a deeply troubling pattern of district governance that, as noted in my previous report, runs throughout the past two years.

Not once in the notes to FOC and CAAC meetings do you see any member of district management deny the claims made in these whistleblower communications. Instead, you see a pattern of ad-hominem arguments directed at the person or persons sending the whistleblower communications by district management, that FOC and CAAC committee members apparently found sufficiently persuasive that they never bothered to examine the veracity of the actual allegations that were made.

Put differently, one of the narratives that runs through the history (so far) of the growing scandal enveloping Jeffco’s Capital Improvement Program is the failure of many members of Jeffco’s key governance committees (the FOC and the CAAC) and the Board itself to exercise their fiduciary duty of care, and the resulting collapse of effective governance processes in a billion dollar organization. This is not unlike similar collapses that occurred in the famous failures of large public companies like Enron and WorldCom.

3 December 2020. Meeting of the Capital Asset Advisory Committee.

From the notes (in the Evidence Appendix):

· “M.L. Richardson stated that she would like the information [provided to the CAAC] to be in one place and in writing. She also stated that it would be helpful to note where the money is from. There are only two sources, bond and associated proceeds and capital transfer funds and accrued interest.

· “Steve Bell said that it has been explained several times that the capital improvement program’s funds come from the bonds issued, any premium obtained and accrued interest. Moneys received from the general fund (capital transfer) are invested and intended to be used towards the end of the Program when bond proceeds have been exhausted. There are two sources of funds to cover unexpected costs they are the built in project contingency and unallocated program contingency.

· “Jeff Wilhite [once again] stated he would like to see how the contingency is being used.

· “Tim Reed stated that the revised Flipbook on the website has some of the information requested.

· “Megan Castle reviewed the Flipbook and thinks the committee needs more information than what has been previously presented.” [Again, this is two years after Prop 5B was passed and the CIP begin spending taxpayers’ and bond investors’ money].

At the 3 December meeting, the CAAC also discussed an email that had been received from Robert Greenawalt.

As described in my 7 October 2020 report, Greenawalt is a retired US Army Colonel. He is a West Point graduate (engineering), with additional masters in Engineering and business administration from the University of Pennsylvania. He also is a certified as a Project Management Professional by the Project Management Institute (a very difficult certification to obtain, requiring a four-year degree, 36 months leading projects, and 35 hours of project management education). Greenawalt has also been the Chief Technology Officer of private sector corporations.

From the meeting notes (available in the Evidence Appendix): “Mr. Greenawalt sent an email with an attachment outlining why he believes a performance audit is necessary. [Note that this email was not provided to CAAC members]. Tim asked the committee if they would like to address Mr. Greenawalt’s concerns or if they prefer the department address them. The committee decided that a response was appropriate but would like the department to draft the response.”

Again, there is no evidence that the CAAC discussed the accuracy of the allegations Greenawalt raised. And once again, as had happened with previous emails from Greenawalt, the CAAC asked the district managers who were the subject of Greenawalt’s complaints to draft a response to him. This makes no sense at all.

Again, from the meeting notes: “M.L. Richardson asked if [Greenawalt] was currently on the meeting. Tim stated that he was advised he could attend in-person but this was not an electronic meeting.”

In fact, many members of district management and the CAAC were actually attending this meeting electronically. Greenawalt had been denied electronic access to the meeting, and told he could only attend in person — at a facility where, because of COVID, the public had no access. Think about that.

3 December 2020 ML Richardson Email (obtained by CORA. Copy in the Evidence Appendix). After the CAAC meeting earlier in the day, M.L. Richardson sent an email to Tim Reed and Steve Bell that was copied to a large number of district staff as well as other members of the CAAC. It included the following:

“At the November 5th CAAC meeting, during discussions regarding the district’s financial auditor, I requested that you ask the auditor for a statement confirming that the money generated from the 2018 bond that has been spent meets the requirements of the bond. Please correct the minutes to reflect this. I had assumed that we would be asked to approve the minutes and that would have been the time for me to make that request. Since preparation of detailed minutes is relatively new for the CAAC, please add an item for review and approval of the minutes on our future agendas so that any corrections or additions can be easily made at that time.”

“Also, on page 3 of the minutes, Jeff Wilhite proposed a review of the bond contingency and volunteered to work on a team to do so…What did staff decide regarding Jeff’s request? Perhaps that request should also be added to our next meeting agenda for further discussion?”

[As you recall, Bell (over whose actions the CAAC is supposed to provide oversight) told Wilhite that he would take the latter’s request (to provide oversight) under consideration. What has been going on at the CAAC for almost two years doesn’t get any more painfully revealing than this].

Back to Richardson’s email to Bell and Reed. “Can you clarify why our meeting was/is not made available to citizens who request to attend virtually?”

“I look forward to the remaining information regarding the bond expenditures that I requested at the November meeting… It appears that other committee members would find this information beneficial as well. I respect that you are of the opinion that all of this information is already available. However, it would be very helpful to have it all in once place… Having this information will assist members of the CAAC in our oversight duty, help us to show that we are good stewards and ambassadors for the school district. In addition, this will help the community to view us as trusted sources of information — especially should another bond opportunity come in the future for Jeffco.”

Again, the critical point is that this email was sent TWO YEARS AFTER PROP 5B WAS PASSED, DURING WHICH TIME THE CAAC WAS SUPPOSED TO BE PROVIDING EFFECTIVE OVERSIGHT OVER THE CAPITAL IMPROVEMENT PROGRAM ON BEHALF OF JEFFCO CITIZENS AND BOND INVESTORS.

5 January 2021. Financial Oversight Committee Meeting. From the notes (available in the Evidence Appendix):

During their discussion of the district’s recent bond issue, Steve Bell made the following remarks: “Bell noted that the coupon rates on the bonds were higher than the capital market environment prefers which enabled Jeffco to issue premium bonds, the same as in 2018. Because of the low rates and coupon demand, the district was able to realize a premium of $68 million on the phase two bonds which will allow the district to expand its capital improvement program.”

The total amount of Bond Premium obtained on the first and second bond issues authorized by the voters who approved Prop 5B is $118,474,497. And that’s before interest earnings on those funds.

Bell apparently assumes that the Board of Education has no say in how Bond Premium will be used.

For example, rather than expanding the CIP, Bond Premium dollars could have been (and what Premium remains might still be) used to reduce the amount of money transferred each year from the district’s General Fund to the Capital Fund to pay for the original Capital Improvement Program.

These additional General Fund dollars could be used to expand programs to recover the substantial COVID learning losses that many Jeffco students have suffered. They also could be used to add staff with clinical training to address the student mental health issues COVID has caused. Or they could be used to address longstanding equity issues in Jeffco (e.g., the Capital Improvement Program failed to include replacement of many low quality school buildings with high percentages of at-risk students).

But Bell apparently believes the Board has no say in this. As noted in my previous report, in other districts (e.g., Denver and Poudre) the board must approve all uses of Bond Premium funds. But not in Jeffco, whose approach to governance is strange, to say the least (equally strange is that unlike in many other districts, in Jeffco the Chief Operating Officer and not the Chief Financial Officer is in charge of the use of bond funds).

Back to the meeting notes. FOC member Mary Everson provided a summary of points raised at the December 2020 meeting of the district’s Audit Committee:

“Everson commented on a correspondence received from a citizen regarding allegations of potential fraud in the capital improvement program. It was noted that the letter was also sent to other individuals in the district and on this committee and others, Board members and CLA.”

“[Steve] Bell advised that the district is pursuing some avenues to resolve the situation and that when information can be shared it will be passed along.” [Does this refer to the Askelson Report?]

“There was discussion regarding the repetitive practice of letters by this individual, past discussions with other members of the committee and staff, discussions at past FOC and Audit Committee meetings, district actions regarding the accusations, and concerns about potential harm to the district. Interim Superintendent Schuh assured the committee that the district is well aware of the accusations and are taking steps to address it.” [Does this also refer to the Askelson Report?]

“Paul Niedermuller with CLA [Jeffco’s independent audit firm] discussed the letter and confirmed that similar correspondence from this individual have been a pattern. He noted that CLA communicated to the FOC that a letter had been received in early fall. He also engaged with Audit Committee members and discussed information around the allegations and clarification on what the audit does.”

“Niedermuller clarified that CLA audits the financial statements whereas some of the allegations and comments within the document are program performance related; thus, he wants to make sure that everyone understands what CLA’s scope of work includes. He confirmed that there have been conversations around this with the district as well as with FOC and Audit Committee. In addition, Niedermuller reiterated that CLA does not engage with the public and will work through the Board or district management in terms of any allegations. He confirmed that the allegations are taken very seriously and that it will look to the district to respond appropriately based upon the items that have been presented.”

[Note that Clifton Larson Allen also audits public companies. These audits are subject to rules set forth by the Public Company Accounting Oversight Board, which takes whistleblower communications extremely seriously. There is no such requirement with respect to school district audits, although one could make the case that when it comes to whistleblower complaints in school districts, Clifton Larson should be following the highest standard to which it is held across ALL its audit/assurance clients. Otherwise, it would in effect be admitting that school districts can get away with treatments of whistleblower communications that would never be tolerated by the general counsel, officers, and board of a public company, or by its auditors and the PCAOB].

Back to the meeting notes. “Staff acknowledged that the concerns raised over the allegations are valid and that information on the response will be shared with the committee when it is available.” NOT THAT THE ALLEGATIONS THEMSELVES ARE VALID. RATHER, “THE CONCERNS RAISED OVER THEM ARE VALID”. THAT’S A CRITICAL DIFFERENCE.

More important points to note:

· District management apparently made no attempt to refute the accuracy of the claims made in the whistleblower correspondence; instead, there were the usual ad-hominem attacks that seem intended to undermine the credibility of the whistleblower, along discussions of “potential harm to the district.” As every trial lawyer knows, if you can’t attack the argument, attack the person making it.

· Billion dollar public companies have very explicit policies and processes for the treatment of whistleblower complaints. Apparently, Jeffco does not.

· Once again, district staff (including Schuh, Stewart, and Bell) made no mention to the FOC about the report that Askelson was working on. And yet again, one has to ask: Why the silence?

· Neidermuller reiterated that CLA had received complaints [PLURAL] about the Capital Improvement Program, and that the FOC had been aware of these complaints [PLURAL] since “early fall.” In point of fact, the FOC has been aware of potential problems with the Capital Improvement Program for longer than that (see my 7 October 2020 Report).

· Neidermuller’s comments are also interesting. After being aware for some time of the whistleblower complaints and allegations about the management and governance of the Capital Improvement Program, why is it that only at the December meeting of the Audit Committee he suddenly felt the need to clarify that CLA has not done an independent performance audit of the Capital Improvement Program?

Also, Neidermuller described CLA’s previous conversations about the Capital Improvement program with the FOC and Audit Committee. Why were these never relayed to members of the CAAC? After all, CFO Nicole Stewart attended all these meetings, and Gordon Calahan is a member of both the FOC and CAAC.

· This lack of communication is particularly curious, given that, at the same time CLA was having conversations about the Capital Improvement Plan with the FOC and Audit Committee, CAAC members were raising questions about whether CLA’s audit met the requirements of Prop 5B.

This last point is critical, given that the CAAC notes show that members of that committee had asked Bell and Reed if the district’s auditor (CLA) could issue a statement that they [the CAAC] were doing what they were supposed to do under Prop 5B (e.g., in the 5Nov20 CAAC notes, ML Richardson and Megan Castle asked if the CAAC could get a note from CLA).

But meeting notes from the 21Jan21 CAAC meeting show that Neidermuller’s comments about the limitations of CLA’s audit — and that it is not a performance audit — were NOT communicated by district management to the members of the CAAC. Again, why not?

7 January 2021. Jeffco Board Meeting, at which it received the regular Quarterly Report from the Capital Asset Advisory Committee. The CAAC presentation was once again given by Steve Bell rather than a citizen member of the CAAC. Bell noted that the total amount of Bond Premium that had been raised in the Capital Improvement Program’s first and second bond issues was $118,474,497.

Bell also noted that construction pricing conditions were still favorable. As well he should have — the Mortenson Index of Construction Costs in Denver increased by only 2.2% in calendar year 2019, and fell by (0.7%) in 2020.

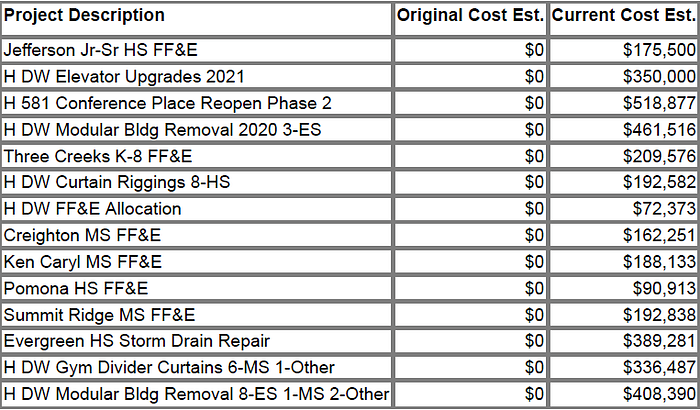

To put this in perspective, the original cost estimate for Capital Improvement Program projects in district run schools, from the 2018 5B campaign flip book, was $563 million ($705m total program cost, less $56m to charter schools, less $86m in program contingency). Applying the two annual construction inflation estimates to $563m yields an estimated cost increase due to inflation of only $8m, to $571 million. That’s a long way away from more than $100 million (so far) in cost overruns and spending on projects that were never disclosed to Jeffco voters during the 2018 Prop 5B campaign.

Also on 7 January, Reed and Bell allowed Tom Murray, a CAAC member attending the meeting, to provide false information to the Board. This happened three times. Not once did Reed or Bell or CFO Nicole Stewart attempt to correct what Murray said.

On three separate occasions, Murray told the board that new projects that were not in the flipbook that voters were given during the 2018 Prop 5B campaign would only be added AT THE END OF THE SIX YEAR CAPITAL IMPROVEMENT PROGRAM IF FUNDS WERE AVAILABLE.

Murray’s statements are available on the board video, and on YouTube at: https://www.youtube.com/watch?v=4h1KH8tbFK0&feature=youtu.be

Murray echoed the statement previously made to the Board by Gordon Calahan, the longest serving member of the CAAC: “This committee was formed to oversee the financial situation of bond issues…that is our primary mission…After the bond has been approved it is very important for us to make sure that each facility gets what it is promised. We cannot make changes to what was promised. Those items that are on the bond have to be followed exactly the way they are, and come in under budget.”

When Murray made his three statements to the Board, was he unaware that the district delivered to the Board on 7 January 2021 a document showing $3.7 million in projects that were not in the original flipbook the district presented to voters during the Prop 5B campaign?

When Murray made his statements, was he unaware of the large number of new athletic facilities that were never disclosed to the voters during the 2018 Prop 5B campaign. These include artificial turf and all-weather tracks at Columbine, Pomona, Standley Lake, Arvada West, Green Mountain, Conifer and Golden High Schools, and new tennis courts at Green Mountain High School?

[Note also that, for all the Jeffco’s claims about the importance of “equity”, with the exception of Pomona HS, all these new athletic facilities have been built at schools with some of the lowest percentages of free/reduced eligible students in the district.]

Finally, did Murray forget about this magnificent new artificial turf field at West Jefferson Middle School in Conifer? That wasn’t in the original 2018 campaign flipbook either…

Was Murray actually unaware of all the new projects not in the original flipbook that have been added to the Capital Improvement Program?

If Murray made his statements in good faith, and really was unaware of all these projects that were never disclosed to voters in the Prop 5B campaign flipbook, what does that tell you about the quality of the CAAC’s “independent oversight” of the Capital Improvement Program over the past two years?

This raises an even more important question: Who in Jeffco Public Schools was responsible for ensuring that the CAAC’s independent oversight obligations created by Proposition 5B were carried out to a high standard?

Obviously, the buck stops with the Board of Education and Superintendent Jason Glass. But it also extends to Kathleen Askelson, the district’s Chief Financial Officer (and later to Nicole Stewart, who replaced her), as well as Craig Hess and Chris Esher, who served as Jeffco Schools’ Chief Legal Counsel during this period. Arguably, it also extends to the Financial Oversight Committee.

The bottom line is that there appear to have been multiple points of governance failure over the past two years, and many people who apparently never attempted to verify the claims made in multiple whistleblower communications. All of these are warning signs of an out-of-control organization that receives a billion tax dollars ever year.

21 January 2021. Citizens Capital Asset Advisory Committee (CAAC) Meeting. CAAC members received a copy of the Askelson Report, but, strangely, did not discuss its contents. The meeting notes (see the Evidence Appendix) state that CAAC members were falsely told that, “The BOE requested and received an interim report on the 2018 CIP prepared by former CFO Kathleen Askelson.”

According to the meeting notes, Bell also stated to members of the CAAC that, “Analysts with the rating agencies congratulated the district on the CIP and how it was being implemented…Steve stated that the analyst pointed that given the scope of work during and what has been accomplished during these times, the management of the 2018 CIP by the Construction Management team was exceptional.”

As I will show in a separate section below, these statements by Bell were very likely false.

4 February 2021. The Jeffco Board of Education, along with Tim Reed and Steve Bell, received a letter of resignation from CAAC member Jeff Wilhite. The letter was obtained via a CORA and is contained in the Evidence Appendix. It states:

“This email is to inform you that I am withdrawing as a member of the Capital Asset Advisory Committee. I have been on the Committee since 2016, specifically being appointed based on my 30 years of construction lending/finance experience and my 15 years of Jeffco charter school board(s) involvement. My decision to withdraw from the Committee is based on what I feel are significant differences between my professional experience in construction project budgeting and funds disbursements, and the processes being used by District staff that are accepted as appropriate by the Capital Asset Committee and the Board of Education.”

The Kathleen Askelson Report: Spin City with Evidence of Election Fraud?

Askelson’s report has many critical and damning flaws. Perhaps the most egregious is that the report exists at all.

Think about it: Why was Kathleen Askelson, the district’s former CFO, who was deeply involved in the Capital Improvement Program for more than three years before her August 2020 resignation, hired by somebody at Jeffco to provide the CAAC, FOC, Board, public, and bondholders with an “independent” review of the CIP?

Was it just a coincidence that her report was requested just two days after Board directors Harmon, Mitchell, Rupert, and Schooley’s rejected director Miller’s motion to conduct an Independent Performance Audit of the Capital Improvement Program?

Was it just a coincidence that Askelson’s report was requested after Greenawalt’s repeated whistleblower emails to the Board, FOC, and CAAC highlighting growing cost overruns and spending on projects not disclosed to voters during the 2018 Prop 5B campaign?

Was it just a coincidence that Askelson’s report was not conducted following the GAO’s procedures for an Independent Performance Audit?

The very existence of Askelson’s report appears to be nothing more or less than an attempt to whitewash of the mismanagement and weak governance of the Capital Improvement Program.

Having spent years as a consultant myself, I also found Askelson’s billing records very interesting.

According to them, she spent less than 8 hours doing the data collection, analysis, and preparation of her report (2.75 hours on 9 November, and some portion of 3.75 hours on 4 December). This suggests three possibilities: (1) Askelson is the most productive consultant in history; (2) Askelson underbilled Jeffco for the actual amount of time she spent working on her report (but why?); or (3) Some other party actually wrote the report, and Askelson only reviewed and edited it.

Another interesting aspect of the Askelson Report story is that Robert Greenawalt is reported to have provided the Jeffco Board of Education (or possibly just its Chair, Susan Harmon) with at least two very detailed critiques of the many erroneous financial claims made by Askelson.

I urge readers of this report to obtain them via CORA. Whether Greenawalt’s analyses of the Askelson Report have been shared in a timely manner with members of the CAAC, the FOC, the Audit Committee, and Clifton, Larson, Allen is unknown. But if it they have not been shared, it is further damning evidence. In a billion dollar public company it would get her removed from her position, and raise questions with the SEC about the timely disclosure of material information.

Reading Askelson’s report, one stunning point jumped off the page for me: Her admission that Jeffco had always intended to spend $2.1 million of the planned $23 million per year of transfers from the General Fund to the Capital Fund to repay Certificates of Participation that had been previously issued to pay for construction of Three Creeks Elementary School and the Expansion of Sierra Elementary School.

Thus, the actual transfer to the Capital Improvement Program over six years that was presented to voters in the Flipbook (and to the FOC and CAAC) was overstated by $12.6 million. AND ASKELSON WAS THE CFO WHO OVERSTATED THE ACTUAL CAPITAL TRANSFER TO THE VOTERS AT THE TIME OF THE 2018 PROP 5B CAMPAIGN!

Serious as this material misstatement is, there is something much worse in the Askelson’s report: The possibility that there may have been election fraud during the 2018 Prop 5B campaign (which only won by a slim margin of 0.24% of the votes cast).

Askelson makes the following damning statement:

“Central sites such as outdoor lab, stadiums and north transportation were not listed in the [2018 Prop 5B Campaign Flip Book, which is included in the Evidence Appendix]; however, the Board of Education was informed these sites were part of the bond program. Meetings with Board members and the Chief Operating Officer occurred May 4–11, 2018, to go over project scope in detail that included these central projects.”

The following chronology of other evidence puts this statement into context:

· On 5 April 2018, the Jeffco Capital Asset Advisory Committee made a presentation to the Board that proposed a $647 million 5 to 7 year Capital Improvement Program (source: Page 2 of 23Aug18 CAAC presentation to the Board; in Evidence Appendix).

** At this 5April meeting, “Staff [was] directed to reevaluate scope, and reduce bond proposal to $567 million (source: Page 3 of 23Aug18 CAAC presentation to the Board).

· 4–11 May, 2018. Meetings between Board members Ali Lasell, Amanda Stevens, Susan Harmon, Ron Mitchell, and Brad Rupert are held with Steve Bell. Per Askelson’s report, “Central sites such as outdoor lab, stadiums and north transportation were not listed in the [2018 Prop 5B Campaign Flip Book, which is included in the Evidence Appendix]; however, the Board of Education was informed these sites were part of the bond program. Meetings with Board members and the Chief Operating Officer occurred May 4–11, 2018, to go over project scope in detail that included these central projects.”

· THIS SECRET AGREEMENT BETWEE BOARD MEMBERS AND BELL WAS NEVER REFLECTED IN ANY BOARD RESOLUTION. NOR WAS THE PLAN TO SPEND CAPITAL IMPROVEMENT PROGRAM FUNDS ON STADIUMS, OR ON ATHLETIC FACILITIES AT COLUMBINE, POMONA, STANDLEY LAKE, ARVADA WEST, GREEN MOUNTAIN, CONIFER AND GOLDEN HIGH SCHOOLS, OR ON THE NEW ARTIFICIAL TURF FIELD AND TRACK AT WEST JEFFERSON MIDDLE SCHOOL EVER DISCLOSED TO JEFFCO VOTERS DESPITE MANY SUBSEQUENT OPPORTUNITIES TO DO SO.

· 23 August 2018 Board Meeting: Proposed resolution “to approve or amend the superintendent’s recommendation for a bond issue question raising funds for school facilities and capital needs across Jeffco Public Schools to be placed on the November 6, 2018 ballot with ballot content to be approved by the Board of Education on September 6, 2018.” The “Pertinent Facts” presented to the public regarding this resolution (see Evidence Appendix) made NO MENTION of the May 2018 meetings.

· 24 August 2018 post on former Superintendent Jason Glass’s “Advance Jeffco” blog (see Evidence Appendix):

- “The Board also put a $567 million bond program on the [November] ballot… Jeffco would use 60% of these funds to bring all schools in the district up to a common standard of quality in terms of instructional space and building safety and security. We would also expand and add career/technical and STEM education facilities and early childhood education options.

- We would use 20% of these funds to reinvest in established parts of Jeffco, keeping those communities and schools attractive places for families and kids. We also have growth areas and would spend 10% of the funds to accommodate new schools and additions where needed. Charter schools would be passed through their proportionate share, 10%.

- Bond funds would also be monitored by a separate blue-ribbon oversight committee and be subject to an annual external audit.”

[Note that Glass’s language here about an annual “external” audit was later made even stronger in Prop 5B which promised voters an annual “independent” audit. One can argue that this implied that it would not be performed by Clifton Larson Allen, the district’s external auditor, which, because of the fees it earns from its existing relationship with Jeffco would not be able to provide an “independent” view on the Capital Improvement Program.]

· 6 September 2018 Jeffco Board meeting. Resolution “to authorize the specific ballot language for Propositions 5A and 5B.” Once again, the detailed “pertinent facts” about the proposed resolution provided by district management to the public did not mention the May 2018 meetings and the secret agreement board members reached with Bell (see Evidence Appendix).

· 7 September 2018 post on Jason Glass’s “Advance Jeffco” Blog:

** On the bond side (funds for construction), the ballot question states asks if the district’s debt can be increased by $567 million, with total repayment costs of $997 million (or a lesser amount) for the purpose of providing Jeffco students, teachers, and staff with a safe learning environment that prepares students for college and the workforce. The ballot language specifies that the bond funds be for these purposes:

- Adding and expanding career/technical education facilities;

- Upgrading safety and security in school buildings;

- Repairing, renovating, equipping, or reconstructing school buildings to ensure all schools are more safe, efficient, and accessible to all students, including those with disabilities;

- Constructing, furnishing, equipping, and supporting needed school buildings and classrooms at all types of schools, including schools chartered by the district.

** The bond language goes to place these conditions on use of bond funds:

- The district will have a preference for hiring local construction contractors;

- The funds cannot be used for senior district administration;

- The spending of these funds is overseen by the citizens’ Capital Asset Advisory Committee;

- The funds are subject to an annual external audit.

Note that Glass fails to mention the other uses of bond proceeds that had been privately agreed by the Board members during the May 2018 meetings described in the Askelson Report. This raises a critical question: DID THE JEFFCO BOARD KNOWINGLY APPROVE BALLOT LANGUAGE FOR PROPOSITION 5B THAT WAS FALSE? AND WHY DID JASON GLASS NOT CORRECT THAT ERROR WHEN HE HAD MULTIPLE OPPORTUNITIES TO DO SO? WHY DIDN’T ASKELSON OR BELL? WHY DIDN’T MEMBERS OF THE BOARD? INSTEAD, DID ALL OF THEM DELIBERATELY MISLEAD JEFFCO VOTERS ABOUT THE PLANNED USE OF TAXPAYER AND BOND FUNDS IF PROP 5B PASSED?

Note also how the original “Blue Ribbon Oversight Committee” (presumably similar to the Bond Oversight Committee used by Denver Public Schools) was changed to the district’s existing Capital Asset Advisory Committee.

The district published the original Prop 5B “Flipbook” for the 2018 Prop 5B campaign, describing how Capital Improvement Program funds will be used, including cost estimates for the projects it would fund at every school (it is included in the Evidence Appendix). Note that under the Conifer Articulation Area, on page 9, there is no “dot” in the box for “Landscaping and Field Improvements” for West Jefferson Middle School.

· 27 September 2018. Watch this “informational video” featuring Jason Glass discussing Proposition 5B. Ironically, he notes that one of the arguments opponents were making against Prop 5B: “Transparency on where these dollars would be spent and how they are accounted for is weak.”

· 5 October 2018. On his “Advance Jeffco” Blog, Jason Glass published “Digging into Ballot Questions: A Look at the Bond (5B)” (copy in Evidence Appendix).

- “Question 5B would allow Jeffco Public Schools to go to the bond market and sell bonds to generate $567 million for construction and other capital improvements (such as furniture or technology). The $567 million would be repaid over a period of 20 years (with interest) through a property tax increase.

- That property tax increase comes to about $1.81 per month, per hundred thousand dollars of residential value. For non-residential property, it’s about $7.28 per month, per hundred thousand dollars of value. The bond’s total repayment (over the 20 years) will be less than $997 million based on language in the ballot question.

- 5B has specific uses written into the ballot question. These include:

- Adding and expanding career/technical education facilities;

- Upgrading safety and security in buildings;

- Ensuring all schools are more safe, efficient, and accessible; and

- Constructing, furnishing, and equipping schools with classrooms of all types in the district.

5B also has some restrictions written into the ballot language. These include:

- Funds cannot be used for senior district administration;

- The spending is overseen by a citizen advisory committee; and

- The funds are subject to an annual external audit.”

Once again, there is no mention of the stadiums, athletic fields and other uses of bond proceeds that had been privately agreed at the May 2018 meetings and were not included in the Prop 5B Flipbook.

·18 October 2018. Colorado Community Media (publisher of the Lakewood Sentinel and other local papers in Jefferson County) endorses Prop 5B:

“Jeffco Public Schools, many parents and educators say, is at a crisis point: It needs money to repair and renovate aging buildings so that all students enjoy an optimum learning environment…Toward that end, Colorado Community Media urges Jefferson County voters to support Ballot Question 5A, a $33 million mill levy override, and Ballot Question 5B, a $567 million bond…

“The bond — which also provides money for charter schools — will pay for renovations and repairs, build new facilities to meet population growth, upgrade security measures, and expand career and technical and early childhood education…

“We applaud the district’s commitment to transparency: A citizens financial oversight committee and independent audit of expenditures will make sure money from the measures is spent as intended. We also commend the district for listening to criticism from its failed bond attempt in 2016, which cited a lack of clarity in how the money would be used. This time, the district has prepared a detailed booklet and website of exactly where the money will go at each school.”

Once again, after reading this endorsement, apparently neither board members Harmon, Lasell, Mitchell, Rupert, and Stevens, nor Glass, Bell, or Askelson attempted to correct the statements made to the public by Colorado Community Media.

In her new report on the Capital Improvement Program, Kathleen Askelson claims that, “The flip book was developed as a marketing tool to enable the community to find their respective schools to see what work was planned and the estimated budget. The flip book was not a comprehensive list of projects.”

But did Harmon, Lasell, Mitchell, Rupert, Stevens, Glass, Bell, or Askelson ever make that clear to Jeffco voters ? Or to the groups advocating for passage of Prop 5B? Or to the editorial board members at Colorado Community Media before they publicly praised “the district’s commitment to transparency” and stressed that “the district has prepared a detailed booklet and website of exactly where the money will go at each school”?

I could find no evidence that they ever did.

When you weigh the available evidence, it raises the very troubling possibility that Harmon, Lasell, Mitchell, Rupert, and Stevens, along with Glass, Bell, Askelson, and possibly other individuals, were engaged in an ongoing conspiracy from May 2018 to the day of the November 2018 election, to deprive the citizens of Jefferson County of their right to honest public service by repeatedly using the district’s flipbook (that they knew to be an incomplete list of the agreed upon CIP projects) to persuade Jeffco voters to pass Prop 5B.

If this is what happened, it goes far beyond poor management and weak governance.

Did the Rating Agencies Really Say What Steve Bell Claims They Did?

The notes to the 21 January 2021 meeting of the Capital Asset Advisory Committee state that, “Steve Bell told members of the CAAC that, “Analysts with the rating agencies congratulated the district on the CIP and how it was being implemented…Steve stated that the analyst pointed that given the scope of work during and what has been accomplished during these times, the management of the 2018 CIP by the Construction Management team was exceptional.”

Based on my ten years of experience at Chase Manhattan Bank, my subsequent experience as a corporate executive, and my wife’s experience as a rating officer at Standard and Poor’s, and later as a public finance banker at Kidder, Peabody, these alleged comments immediately struck me as highly unusual language coming from a credit analyst.

There is a logical reason for this. When you make a loan or purchase a bond and hold it to maturity, your upside is limited to the interest you earn. In contrast, if the issuer defaults, you can forgo interest and lose all your principal. In contrast, when you purchase an equity (i.e. a share of stock), your upside is unlimited (e.g., just ask early investors in Amazon), while if the company goes out of business your downside is limited to losing the price you paid for the stock.

As a group, credit analysts are therefore a much more sober and less enthusiastic lot than equity analysts. More specifically, credit analysts (which include analysts at credit rating agencies like Standard and Poor’s and Moody’s) are not given to congratulating issuers on the management of their capital improvement programs.

And so I filed a CORA asking Steve Bell to name the credit rating agencies and analysts he quoted in his comments to the CAAC. Unsurprisingly, Jeffco refused to answer my question (included in the Evidence Appendix).

I also reviewed the Credit Reports published by S&P and Moody’s after their meetings with Bell and Nicole Stewart. Both are included in the Evidence Appendix. Neither contains the comments about the Capital Improvement Program that Bell claims they made.

Finally, I reached out to S&P and Moody’s to see if they had issued any other reports that contained the statements that Bell claimed they made. Both said there were no other reports. S&P also stated “there is no commentary regarding ‘congratulations’.” This correspondence is also included in the Evidence Appendix.

The weight of evidence suggests that Steve Bell either grossly misrepresented or fabricated the statements he claims the rating agencies made about Jeffco’s management of a Capital Improvement Program that was already more than $100 million over budget at the time Jeffco met with them.

Bell’s claims about the rating agencies’ comments were made to both the CAAC and, possibly, to the FOC (it is hard to definitively tell from the latter’s meeting notes), both of which are advisory committees to the board of a billion dollar school district. The notes from the CAAC meeting are also available to the public and to investors in Jeffco’s bonds.

In a billion dollar public company, concerns about the truthfulness of statements made to these parties by the Chief Operating Officer would, at minimum, cause the board to retain outside legal counsel to investigate what happened. And if the statements were found to be false, Bell would be fired for cause.

But in the billion dollar school district that is Jeffco? So far, nothing.

Conclusion

The title of this report says it all. Since my last report was published on 7 October 2020, the scandal enveloping Jeffco Schools’ out of control $705 million Capital Improvement Program has widened and worsened.

It also seems that possible efforts to cover up this scandal have grown more desperate and brazen, even as the Capital Improvement Program’s cost overruns and spending on projects not disclosed to voters in 2018 have increased exponentially, to more than $100 million today. On the horizon is the complete squandering of $118 million in Bond Premium funds the district received.

For me, by far the most shocking statement in Kathleen Askelson’s report was her description of the May 2018 private meetings between Steve Bell and Board members Harmon, Lasell, Mitchell, Rupert, and Stevens in which they agreed to include in the Capital Improvement Program spending on projects that were never disclosed to voters during the 2018 Proposition 5B campaign.

Prop 5B barely passed by the thinnest of margins, only 1,047 votes, or 0.24% of the total votes cast.

If plans to use bond funds for stadiums, tracks, artificial turf fields, and tennis courts at a number of affluent schools had been disclosed to Jeffco voters in 2018, does anybody reading this doubt that Prop 5B would have failed?

A review of the evidence shows that there were many opportunities for board members and district leaders to rectify the failure of the district to disclose all planned Capital Improvement Program spending, to include what Board members and Steve Bell had agreed at their private May 2018 meetings. Time and again these opportunities were ignored (e.g., in the flipbook, Jason Glass’s repeated statements, and following Colorado Community Media’s endorsement of Proposition 5B).

This suggests that something much darker than anybody previously suspected may have been afoot in Jeffco.

The most recent evidence, in combination with the previous evidence in my 7 October 2020 report, provides further support for the claim that multiple management and governance processes have repeatedly failed in Jeffco over the past three years. It also provided further evidence of the district’s deeply dysfunctional culture, and, it would seem, rot at the top.

And don’t forget that the crisis in the Capital Improvement Program has emerged while the district’s overhead costs were increasing by $48 million, and academic achievement results were in an accelerating decline, in my view due to the same underlying root causes.

In a billion dollar public company, multiple failures like this would trigger a crisis, including media investigations, inquiries and possible action by the Securities and Exchange Commission, and possible litigation by shareholders against the board of directors.

But in Jeffco? An apparent coverup.

Jeffco’s voters and bond investors have been badly let down — to put it mildly.

It is therefore long past time for the Jeffco Board of Education (whether the current one or a new one elected in November 2021) to retain outside advisors to conduct:

(1) An independent performance audit of the Capital Improvement Program, in compliance with Government Auditing Standards, with detailed recommendations and implementation plans to fix any problems found (including the potential replacement of members of the FOC, CAAC, the district management team, and CLA as the Jeffco’s independent auditor);

(2) An independent review of Jeffco’s financial controls, and management decision, whistleblower, and governance processes, to identify failures in these areas as they relate to the Capital Improvement Program, as well as detailed recommendations and implementation plans to fix any problems found (including the potential replacement of members of the FOC, CAAC, the district management team, and CLA as the Jeffco’s independent auditor).

Doing nothing ensures that the consequences of Jeffco’s poor management, weak governance, and dysfunctional culture will only grow worse. And our children will pay the price.

DOWNLOAD THE EVIDENCE APPENDIX

Tom Coyne is a business executive, former member of the Jeffco District Accountability Committee, and former Chair of the Wheat Ridge High School Accountability Committee. His writing about Jeffco Schools, Colorado, and national K12 education issues can be found at https://tcoyne.medium.com. His wife, Susan Miller, was elected to the Jeffco Board of Education in November 2019. These are solely Coyne’s views.

Coming soon: Jeffco Schools’ Out of Control $705 Million Capital Program, Chapter Three: The Arrogance of Power